Closing the lending data gap with cash flow analytics

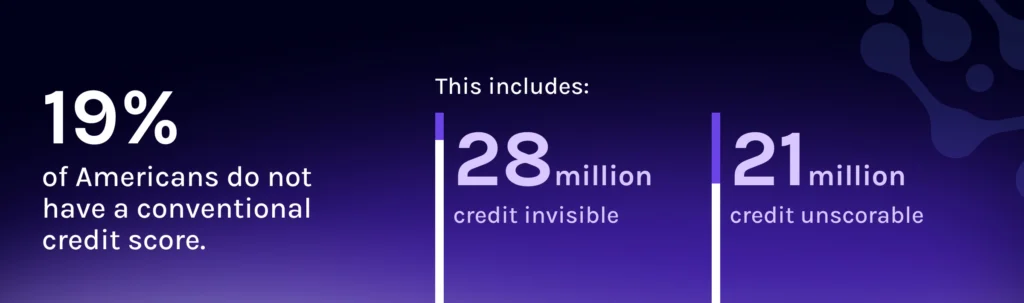

According to a 2022 Consumer Financial Protection Bureau (CFPB) report, nearly 50 million U.S. adults are credit invisible or unscorable. That’s roughly one in five Americans. For lenders, this creates a persistent challenge: how do you assess a borrower’s creditworthiness when traditional credit bureau data comes up short?

This challenge becomes more complex during periods of economic volatility. Events like the COVID-19 pandemic, shifts in the job market or rising inflation can quickly render historical credit data obsolete. With changing income patterns and rising participation in gig work, relying solely on backward-looking credit scores is no longer enough.

In a recent live session, Ocrolus SVP of Growth David Snitkof joined Chris Hansen, GM of Cash Atlas Solutions at Nova Credit, to explore how real-time cash flow analytics are reshaping underwriting strategies and empowering lenders to bridge the data gap.

How economic events disrupt traditional underwriting

Economic shocks can alter a consumer’s financial picture almost overnight. A borrower who once had a high FICO score and reliable income may experience unexpected job loss or reduced hours, undermining their historical creditworthiness.

Traditional underwriting models, which primarily depend on credit bureau data, are ill-equipped to respond to these abrupt changes. Hansen explained, “The access component is a means to the end of, ‘what are the analytics that I can actually drive to have more predictability in my portfolio?’”

Cash flow analytics offer a dynamic alternative. By analyzing bank transactions, income streams and recurring expenses, lenders gain a near real-time view of a borrower’s financial health. This insight enables more accurate risk assessment, particularly when past data no longer tells the full story.

Closing the lending data gap with better insights

Cash flow analytics don’t just supplement traditional credit data—thdo aey help complete the picture. By integrating both third-party credit data and first-party data submitted directly by borrowers, lenders can evaluate applicants more holistically.

As Snitkof emphasized, “Having tools, not just the raw data but analytics to be able to analyze the income and the cash flow, really gives you a better picture of the customer’s financial life.”

This approach benefits lenders and borrowers alike. Lenders can confidently assess applicants who may have thin or no credit files, while borrowers are evaluated on their current financial realities rather than outdated credit histories.

Additionally, cash flow analytics allow lenders to scale personalization and inclusion. By embracing a broader set of data sources, lenders can tailor financial products to better suit each borrower’s needs, whether they’re gig workers, recent immigrants or recovering from a financial shock.

Moving toward smarter, inclusive lending

In a volatile economy, traditional models fall short. Real-time cash flow analytics empower lenders to lend with confidence, even in the face of uncertainty. By using cash flow insights in tandem with traditional credit data, lenders can:

- Make better-informed lending decisions

- Reduce risk across portfolios

- Expand access to credit for underserved populations

To learn more about how your team can implement real-time cash flow analytics, watch the full live session or book a demo with Ocrolus today.

Key takeaways

- Real-time cash flow data gives lenders a better view of a borrower’s income and ability to repay in unpredictable markets.

- Lenders must use both third-party (credit bureau) and first-party (borrower-submitted) financial data to close the information gap.

- Tools that make it easier for borrowers to share data improve underwriting decisions and borrower experience.