The hidden friction in small business funding (and why it hurts everyone)

TL;DR: Hidden friction in small business funding shows up as slow cycles, fragile trust and inconsistent files. Standardizing intake and cash-flow analytics with an AI-powered platform delivers verified, underwriting-ready data, reduces rework and speeds approvals, so more qualified deals get funded faster without adding headcount.

Small business funding should be straightforward. Lenders want to approve more good loans, brokers want to place deals efficiently and borrowers need capital to grow. Yet despite new tools, persistent friction slows funding cycles and leaves qualified deals unfunded. This hidden friction does not just frustrate one party. It weakens the entire ecosystem of a loan.

The cost of slow small business funding

The modern business moves fast, but funding often crawls. What should take days stretches into weeks as teams chase documents, resolve mismatches and rekey information. The result is a gap between opportunity and capital access. Borrowers miss windows to buy inventory, lenders risk losing customers to faster competitors and brokers spend cycles on status checks instead of placing the next deal.

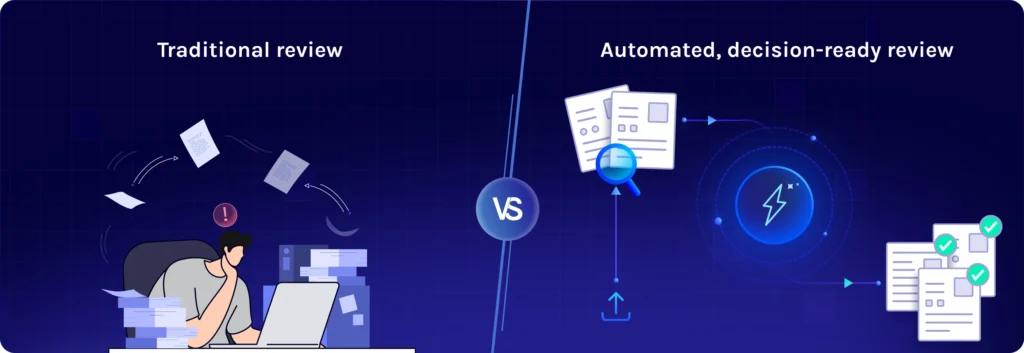

You can close this gap by moving away from manual review and toward automated, standardized loan files for review. AI-powered document automation removes repetitive steps that stall underwriting. With document automation, lenders accept bank statements, invoices, tax forms and other artifacts in many formats, then extract, normalize and validate the data in a consistent workflow. Pair that with cash-flow analytics and teams get standardized income, balance volatility and anomaly insights that shorten time to decision.

Faster cycle time raises pull-through, protects rate locks and helps brokers win repeat business.

Trust breaks when data isn’t consistent

Trust underpins broker, lender and borrower relationships, but legacy processes often erode it. Emailing sensitive PDFs invites confusion about versions and chain of custody. Unclear routing creates fear of backdooring, where a broker worries a lender might approach a borrower directly. Fragmented systems mean inconsistent status updates and duplicate requests, which frustrate everyone.

A trust AI data and analytics platform can help to rebuild trust by standardizing how information moves and how it is verified. With income verification, lenders can validate cash flows and statements against secure sources so brokers know the exact artifacts needed and get transparent progression from upload to analysis to decision, which reduces surprises and defensiveness.

Consistent, tamper-evident data flows reduce second-guessing and the compensating controls that slow deals. Trust improves when documents and analytics move through a double-consent, role-based workflow with tamper-evident records. No backdooring, no version roulette.

Standardized cash-flow analytics speed decisions

The most overlooked friction point is inconsistency. One lender’s “complete” file is another lender’s rework project. Bank statements arrive in different layouts. Transaction categorizations vary. Key fields are mislabeled or missing. Without a common language for underwriting, every file becomes a one-off.

Automated document classification and analytics establish that common language. Using document automation to classify and extract followed by cash-flow analytics to structure and interpret, lenders receive standardized data that aligns to internal policies. Brokers benefit because a standardized checklist and output format raises conversion across their lender network. Borrowers get a predictable experience regardless of which lender ultimately funds the deal.

When brokers and funders exchange the same verified cash-flow metrics and tamper-evident artifacts, a decline doesn’t restart the process. Files port across trusted counterparties with zero rework, preserving momentum for qualified borrowers and protecting everyone’s time.

What better looks like for lenders, brokers and borrowers

Speed, trust and consistency are interconnected. Improving consistency increases trust because everyone is working from the same verified data. More trust reduces the need for compensating checks, which speeds up decisions. Faster decisions boost pull-through and improve borrower satisfaction. The benefits compound across lenders, brokers and borrowers, which is how a market grows.

For examples of impact, explore how leading lenders have modernized operations using Ocrolus. See the Kapitus customer story for a look at how standardized cash-flow insights and automation yield faster, more confident decisions.

What doing better looks like

Imagine every submission arriving decision-ready, mapped to your underwriting policies, with clear flags for anomalies or missing items. Brokers would place deals with confidence because intake is transparent and requirements are unambiguous. Borrowers would see fewer repeat requests and faster outcomes. Lenders would increase funded volume without adding headcount because analysts spend time on exceptions, not on formatting and reconciliation.

Key takeaways

- Slow cycles, fragile trust and inconsistent files are the real costs of SMB funding friction.

- Digitized intake + standardized cash-flow analytics produce verified, underwriting-ready data.

- Network-level consistency raises pull-through and reduces rework across lenders and brokers.

- Verified, consistent data builds trust without extra checks.