SMB trends: Increases in AI use and non-traditional funding amid economic uncertainty

Ocrolus and OnDeck recently unveiled the latest installment of the Small Business Cash Flow Trend Report, delivering valuable insights on U.S. small business trends and sentiment from Q1 2025.

The report is based on responses from 437 small businesses with working capital loans from OnDeck and draws from cash flow data across more than 2 million small business financing applications processed by Ocrolus. While optimism for future growth remains strong overall, tariff uncertainty and shifting credit access are beginning to shape small business behavior.

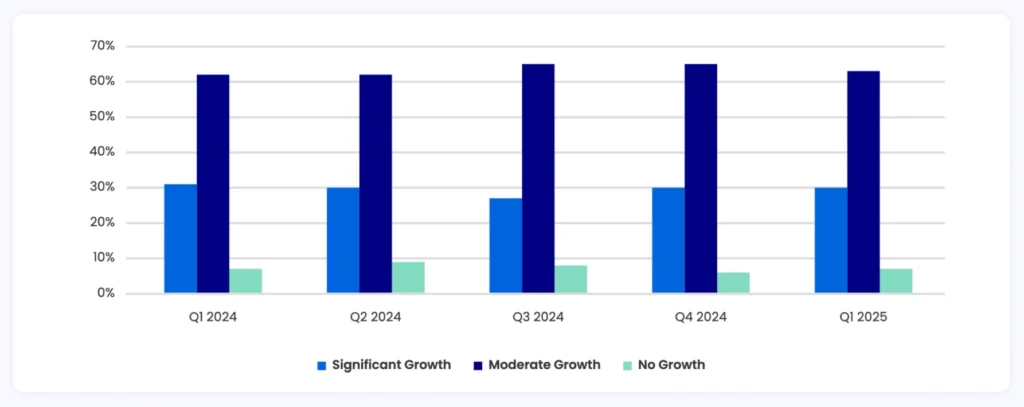

Future growth expectations

AI use in small businesses in 2025

One of the most notable takeaways is the sharp increase in AI use among small businesses. The report shows that 69% of small business owners are now using AI tools often to assist with marketing-related tasks, and 17% are doing so daily or weekly.

Top use cases include:

- Content generation

- Email writing and personalization

- Campaign performance optimization

Beyond marketing, SMB operators are beginning to experiment with AI for expense management, demand forecasting and even customer service automation. Ocrolus has long been a proponent of scalable AI-enabled lending operations, particularly during times of macroeconomic uncertainty when automation supports faster decision-making and reduced overhead.

Tariff pressures reshaping SMB strategies

Based on February 2025 survey responses, prior to the March tariff announcements, 27% of small business owners said new tariffs could negatively impact their operations. That number rises to 47% among manufacturers, who depend on cost-sensitive raw materials.

Only 8% of businesses reported expecting any positive impact from tariffs.

More than half of SMBs (55%) said they’re actively preparing to respond, with 36% planning to pass increased costs onto customers. Others are exploring options like reshoring supply chains, sourcing alternative vendors or deferring planned expansions.

For SMB lenders, this signals growing sensitivity to input costs and volatility. Lenders must account for the operational fragility tariffs may expose.

Traditional bank reliance hits an all-time low

In Q1 2025, the trend away from traditional banks accelerated. A record-high 76% of small businesses bypassed applying to traditional banks in favor of non-bank lenders.

Why?

- Anticipated denial (especially for younger firms)

- Paperwork burdens and slow underwriting

- Interest rate rigidity

Among businesses operating for 16+ years, 42% reported being denied by traditional banks. For those in the 6–10 year range, denial rates rose 16% compared to Q4 2024.

Supporting this shift, Ocrolus data shows a 34% year-over-year drop in bank loan inflows and a modest 1% rise in fintech inflows. These results underscore that businesses increasingly prefer faster, more accessible lending options, even if traditional terms remain available.

To compare with prior insights, view the Q4 2024 report.

How cash flow analytics equip lenders in volatile times

In a climate where SMBs are navigating price shocks and fluctuating demand, lenders must go beyond FICO scores to assess true borrower risk. Ocrolus’ cash flow analytics enable lenders to analyze real-time banking behavior, such as income volatility, expense trends and NSF frequency, directly from borrower statements.

These insights empower underwriters to:

- Identify red flags early, like unstable revenue

- Surface positive cash flow trends, even without strong credit history

- Confidently price loans in high-risk environments

Automation is key here. Ocrolus enables AI-driven underwriting workflows that reduce manual review, increase consistency and support better decisioning when volatility rises.

Despite a complex operating environment, small businesses continue to innovate, by adopting AI tools, reassessing sourcing and embracing fintech lending options. Lenders that pair speed with accuracy and transparency will be best positioned to serve them.

View the full Small Business Cash Flow Trend Report here for more insights on how SMBs are adapting.

Key takeaways:

- 76% of small businesses bypassed traditional bank applications, citing friction and denial fears

- 69% of SMBs are using AI, primarily for marketing content and emails

- 55% of small businesses are preparing for tariff impacts, with 36% planning to pass costs to customers

- Ocrolus’ cash flow analytics provide real-time visibility into borrower health, critical for lenders operating in volatile markets