Docs-to-digital bank statement analysis: how SMB lenders fund faster with fewer surprises

TL;DR: Manual bank statement review costs SMB lenders 30+ minutes per matching task, and document manipulation still slips through. Docs-to-digital bank statement analysis — automatically reconciling submitted PDFs against immutable digital transaction data and ranking mismatches by severity — improves fraud detection, collapses pre-funding review and reduces the need for more underwriting headcount during high-volume periods. It is the emerging industry pattern for funding more applications with fewer surprises and it is reshaping how small business funding teams allocate analyst time.

Small business lenders lose time and money on one of the oldest problems in underwriting: deciding whether the bank statement a borrower uploaded actually matches what is happening in that account. Each manual matching task — opening two windows side by side to compare totals, transaction dates and counterparties line by line — costs an analyst 30+ minutes per application, and that assumes the statement is legitimate. Manual “stare-and-compare” review is the weakest link in the fraud-prevention chain: slow on a good day, error-prone on a bad one. As application volume scales and fraud patterns get more sophisticated, the workflow itself is becoming the liability.

Why the stare-and-compare workflow stopped working

Bank statements remain the backbone of small business underwriting. They capture revenue, deposits, NSFs, balances and the operating patterns that predict repayment. But the format is a headache: PDFs are easy to manipulate, layouts vary across thousands of institutions and a human reviewer can only spot so many discrepancies before fatigue sets in. Document manipulation — altered balances, inserted deposits, spliced statement pages — remains one of the most common concealment methods in small business lending fraud, and it is the kind of tampering a manual reviewer is least equipped to catch on a tight pre-funding clock.

At the same time, application volume keeps climbing. Fintech-era SMB lenders now routinely process tens of thousands of applications a month. A workflow that asks an analyst to eyeball three PDFs per borrower cannot scale with the pipeline without adding headcount — and during peak funding windows, even a well-staffed team will see accuracy degrade and the pressure to bring on more underwriting resources mount.

Digital bank data alone does not close the gap

Open banking has been billed as the answer. Pull transaction data directly from the borrower’s account through an aggregator, the pitch goes, and there is no need to trust an uploaded PDF. The reality is messier. Bank-linking flows have meaningful connection failure rates, credentials expire and the digital feed often returns only 90 days of history when underwriting requires 12 months. Borrowers also legitimately hold accounts at institutions that aggregators do not cover well.

The industry has settled into a docs + digital posture — accept whichever format the borrower can provide, and merge the two sources on the back end. That posture solves the collection problem. It does not solve the reconciliation problem. Analysts still have to decide, application by application, whether the uploaded document agrees with the digital feed or whether the discrepancies warrant a second look.

What docs-to-digital bank statement analysis actually does

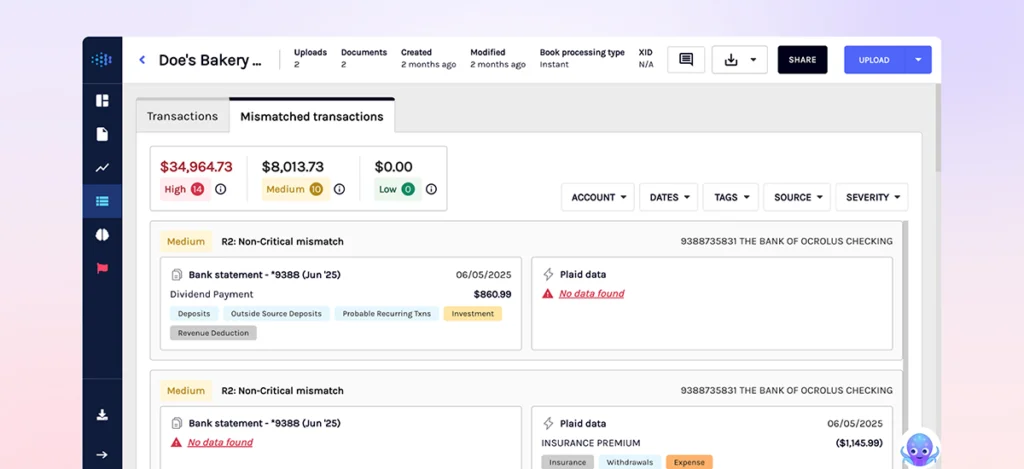

The emerging industry pattern — increasingly referred to as docs-to-digital bank statement analysis — is to automate the reconciliation itself. Software compares each transaction on the uploaded PDF against the corresponding entry in the digital feed and surfaces every mismatch — missing deposits, altered amounts, counterparties that do not line up. Severity scoring ranks discrepancies by risk so NSFs, undisclosed loan payments, crypto activity and gambling-related transfers rise to the top, while benign formatting differences are filtered out. Each borrower application gets a book-level summary instead of a stack of exceptions for an analyst to manually sort through.

Ocrolus is one platform building against this pattern with its Docs-to-Digital capability, which reconciles uploaded statements against Plaid data and returns severity-scored results in seconds. Other vendors are developing similar flows. The structural shift is what matters: pre-funding review moves from an open-ended document comparison to a focused exception workflow, and the gains show up in three places — analyst time drops because reviewers reclaim 30+ minutes per matching task and only touch the applications that actually warrant a second look, fraud detection improves because every PDF is reconciled against an immutable digital source instead of eyeballed under fatigue and lenders can absorb high-volume periods without immediately scaling underwriting headcount because exception cases — not every application — are what consume reviewer time.

Combining uploaded documents with live bank data is no longer optional in small business funding. Open banking will continue to expand, but documents are not going anywhere and borrowers will keep choosing the data-sharing path that feels easiest to them. The lenders pulling ahead are the ones that stopped asking “docs or digital?” and started asking how fast they can reconcile both. Docs-to-digital bank statement analysis is how they answer that question, and it is quickly becoming table stakes for any SMB lender trying to fund more applications with fewer surprises and without expanding the review team. It also sets the foundation for the next phase of underwriting automation, where agentic AI workflows orchestrate document collection, reconciliation and cash flow analysis as a single decision pipeline.

Key takeaways

- Manual bank statement matching costs analysts 30+ minutes per task and no longer scales with SMB lending pipeline growth or with modern fraud patterns.

- Open banking alone does not close the gap — borrowers still upload documents, aggregator coverage is partial and digital feeds often return limited history.

- The industry “docs + digital” posture solves data collection but leaves analysts reconciling two sources manually, application by application.

- Docs-to-digital bank statement analysis — automated reconciliation with severity-scored mismatches against immutable digital sources — is the emerging pattern replacing stare-and-compare review at volume.

- Ocrolus Docs-to-Digital is one implementation of the pattern, saving 30+ minutes per matching task, improving fraud detection by reconciling uploaded statements against immutable Plaid data and reducing the need for additional underwriting headcount during high-volume periods.

FAQs

What is bank statement reconciliation in small business lending?

Bank statement reconciliation is the process of comparing the transactions listed on a borrower-submitted bank statement against an independent source — typically a digital transaction feed pulled from the borrower’s bank account — to confirm that deposits, withdrawals and balances line up. It is how SMB lenders verify that the document they are underwriting actually reflects the account’s real activity.

Why does open banking not solve the problem on its own?

Open banking provides tamper-resistant transaction data but comes with real limitations. Connection failure rates can be meaningful, borrowers drop out of bank-linking flows, credentials expire and the digital feed typically covers a shorter window than underwriting requires. Most SMB lenders still rely on uploaded documents to fill those gaps, which means both sources need to be reconciled.

What is a “docs + digital” approach to underwriting?

Docs + digital is the practice of accepting both uploaded financial documents and digital bank connections from borrowers, then using whichever data source — or combination of sources — provides the most complete picture for a credit decision. It is now standard across most fintech-oriented SMB lenders.

What is docs-to-digital bank statement analysis?

Docs-to-digital bank statement analysis is the automated reconciliation of a borrower’s uploaded bank statement PDF against the corresponding digital transaction feed pulled from their account. The software compares every transaction across both sources, flags mismatches by severity and returns a single, reviewable summary — replacing manual stare-and-compare review with a focused exception workflow.

How does automated reconciliation catch fraud?

Automated reconciliation compares every transaction on a submitted bank statement against the corresponding digital record. When deposits, balances or counterparties in the document do not match the immutable digital feed, the system flags the discrepancy — surfacing document manipulation, omitted transactions or inflated revenue that a manual reviewer would likely miss on a tight clock.

What are the business benefits of automating pre-funding review?

Lenders see three compounding effects: analyst time drops by 30+ minutes per matching task, fraud detection improves because every uploaded PDF is reconciled against an immutable digital source instead of eyeballed under fatigue and the same review team can absorb high-volume periods without scaling underwriting headcount because only exception cases consume reviewer time.