Why repeat lending demands a full history of business cash flow

TL;DR: Small business lenders frequently fund the same merchants multiple times, but most underwriting platforms analyze each application in isolation. This post explains why a full history of business cash flow — one that spans multiple applications and funding cycles — is a material advantage in repeat borrower underwriting, fraud detection and portfolio risk management. Ocrolus enables lenders to query a business’s complete cash flow history across all prior submissions, replacing manual workarounds with structured, queryable data.

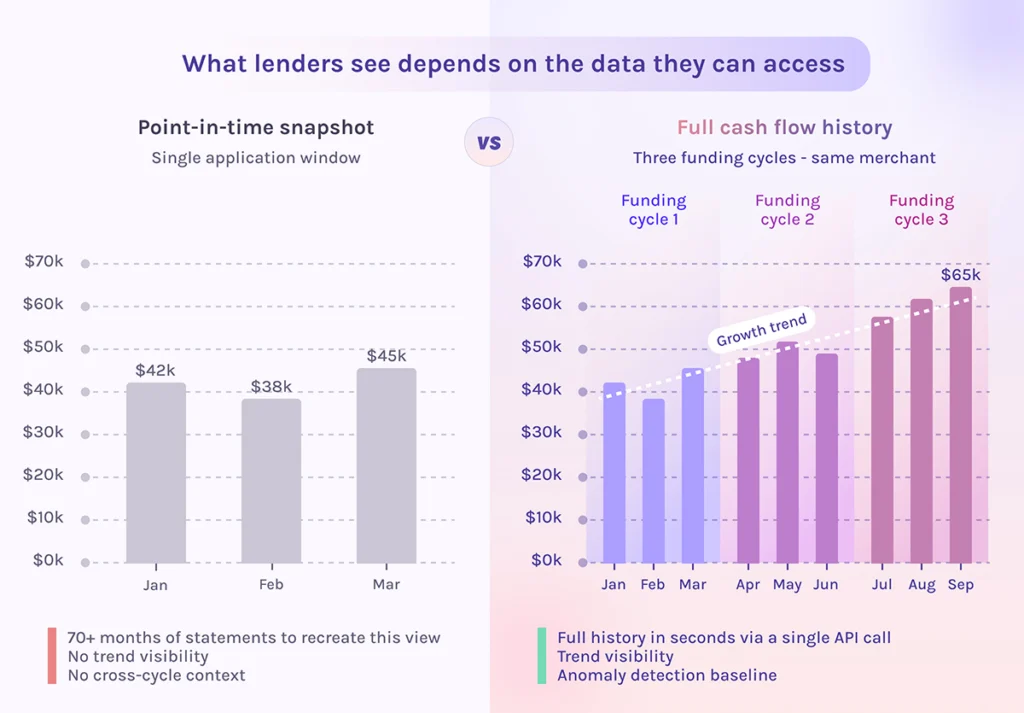

Most SMB lenders work with the same businesses more than once. A merchant gets funded, performs, comes back for working capital six months later and returns again the following year. Each application is a new credit event — but it isn’t a new relationship. The problem is that underwriting infrastructure rarely reflects that reality. Each submission gets analyzed in isolation, producing a snapshot of cash flow at a single point in time. The history that exists — every prior submission, every period of performance across previous funding cycles — sits fragmented across separate workflows. Underwriters have to piece the story together manually, which means they often don’t have the full picture when it matters most.

How lenders track repeat borrower history today — and why it breaks

The manual patches lenders have built to compensate are telling. Some funders upload 70 or more months of bank statements into a single oversized book to generate multi-period analytics for a repeat merchant — a workaround that creates significant processing latency and still requires manual management. Others maintain spreadsheets, manually reconciling analytics exports application by application to approximate a view of borrower history. These approaches work until they don’t. They’re labor-intensive, error-prone and difficult to scale.

A spreadsheet tracking a merchant’s last three funding cycles tells you what happened. It doesn’t automatically surface whether average daily balances are deteriorating, whether revenue consistency has declined between applications or whether an anomaly in the most recent submission conflicts with prior data. The Federal Reserve’s Small Business Credit Survey consistently finds that repeat lending relationships are central to how SMBs access capital — yet the analytical infrastructure to support those relationships often hasn’t kept pace with the volume of repeat applications lenders are processing.

The manual stitching problem also compounds at scale. A lender with a large book of repeat borrowers can’t maintain that institutional knowledge reliably without dedicated infrastructure. Smarter SMB underwriting depends on having the right data infrastructure underneath it — not just better analysts working harder with incomplete information. The underwriter on a renewal may not be the one who worked the original deal. Context gets lost. Decisions get made without the full historical picture that would have sharpened them.

What a business’s full cash flow history reveals that a snapshot can’t

Access to a business’s full cash flow analysis history across applications changes several things at once.

Trend visibility is the most direct benefit. Instead of evaluating a business against its own recent performance in isolation, underwriters can see whether cash flow has grown, compressed or become more volatile relative to prior funding cycles. A merchant showing strong current revenue but deteriorating consistency compared to six months ago is a different risk than one showing steady, modest growth — and that distinction doesn’t surface in a single-application analysis.

Fraud detection improves as well. Patterns that look clean in isolation — regular deposits, reasonable expense ratios, plausible revenue — can look very different against prior submissions from the same merchant. Anomalies in reported revenue, unusual shifts in account behavior or inconsistencies between applications become visible only when you have a historical baseline to compare against. For SMB lenders managing fraud risk, that baseline is often the difference between catching a manipulated submission and missing it entirely.

Repeat borrower assessment also becomes more structured. Lenders evaluating renewal requests can move from a gut-check on relationship history to a data-driven review of how a business has actually performed across every credit event on record.

How cash flow history over time strengthens SMB portfolio decisions

The implications extend beyond individual underwriting decisions. Lenders managing a portfolio of SMB relationships face a concentration and performance trend problem that point-in-time cash flow data isn’t equipped to solve. If a segment of the portfolio is concentrated in merchants whose cash flow has been deteriorating across successive applications, that’s a portfolio-level signal — but only if the data infrastructure exists to surface it.

A full cash flow history also enables more precise renewal pricing. A merchant with consistent cash flow growth across four funding cycles is a meaningfully different risk than one with volatile performance and a strong current snapshot, even when the most recent bank statements look similar. Risk and data science teams benefit too — programmatic access to transaction-level history across multiple funding cycles is the foundation for building and validating credit models without manual data preparation.

Structured access to historical cash flow data is where lenders are beginning to build a real analytical edge. The Ocrolus platform enables lenders to retrieve a business’s complete cash flow history — deduplicated transactions and summaries across all prior submissions — in seconds rather than processing 70+ months of statements manually. Analyst effort shifts from reconciling data to making decisions. As repeat borrower books grow and competition for quality SMB relationships tightens, that shift becomes a structural underwriting advantage. Schedule a demo today to get started.

Key takeaways

- Most SMB lending is repeat lending, but underwriting tools are still built around single-application, point-in-time cash flow snapshots.

- Lenders have developed manual workarounds — combined workbooks, tracking spreadsheets — that can’t scale and fail to surface automated trend analysis.

- A full view of cash flow history improves underwriting across three dimensions: trend visibility, fraud detection and structured repeat borrower assessment.

- Portfolio risk management improves when lenders can track cash flow performance patterns across funding cycles, not just at the moment of each application.

- Lenders with structured access to historical cash flow data have a compounding analytical advantage as their repeat borrower books grow over time.

FAQs

Why do lenders need a full history of business cash flow?

Analyzing a business’s cash flow across multiple applications and funding cycles — rather than at a single point in time — gives lenders a far richer picture of risk. It means comparing how a merchant’s revenue, average daily balance and cash flow consistency have changed over time, not just assessing the most recent bank statements in isolation.

Why do SMB lenders need more than a point-in-time cash flow snapshot?

A single cash flow snapshot reflects how a business looks today. It doesn’t reveal whether performance is trending up, deteriorating or becoming more volatile over time. For repeat borrowers — who make up a significant share of most SMB portfolios — the trajectory across multiple applications is often more predictive of repayment risk than any single snapshot.

How does historical cash flow data improve fraud detection?

Fraud patterns that appear clean in a single submission often break down when compared against a merchant’s prior application history. Inconsistencies in reported revenue, unusual shifts in account behavior or discrepancies between applications are only detectable when a lender has a baseline to compare against. Without the full submission record, a manipulated document may pass review simply because it looks internally consistent — even if it conflicts with prior data from the same merchant.

What’s the difference between cash flow history and a standard cash flow analysis?

A standard cash flow analysis produces a snapshot: revenue, expenses, average daily balance and cash flow metrics for a defined period. Cash flow history layers multiple snapshots over time, enabling lenders to identify trends, flag anomalies relative to prior submissions and assess consistency across funding cycles — none of which are visible in a single analysis.

How can lenders access a business’s cash flow history across multiple applications?

Lenders using Ocrolus can retrieve a merchant’s complete cash flow history — deduplicated transactions, cash flow summaries and entity data — across all prior submissions through a single API call. This replaces the need to upload 70+ months of statements into an oversized book or manually reconcile exports across spreadsheets. The result is historical analytics available in seconds, with no re-integration required for lenders already using Ocrolus analytics.