Smarter SMB underwriting starts with better intelligence

TL;DR: Ocrolus Intelligence brings network-level borrower behavior and industry benchmarking directly into SMB underwriting workflows. By combining loan inquiry velocity with peer-based financial context, lenders can identify stacking risk earlier, validate assumptions faster and make more confident credit decisions without adding manual research steps.

Speed in small business funding is rarely limited by decision-making skill. More often, it breaks down because underwriters are forced to evaluate merchants in isolation, relying on raw cash flow numbers and borrower-provided disclosures with limited external context.

Ocrolus Intelligence was built to close that gap. Announced during Ocrolus’ January Product Pulse, Ocrolus Intelligence introduces network-level insights directly inside every SMB Book, giving lenders real-world context drawn from hundreds of thousands of applications processed each month.

Rather than asking underwriters to leave their workflow or consult separate tools, Ocrolus Intelligence embeds borrower behavior signals and industry benchmarks directly alongside cash flow analytics in the Ocrolus dashboard and API.

Loan inquiries reveal borrower behavior in real time

One of the core components of Ocrolus Intelligence is loan inquiries, a new capability purpose-built for SMB lending.

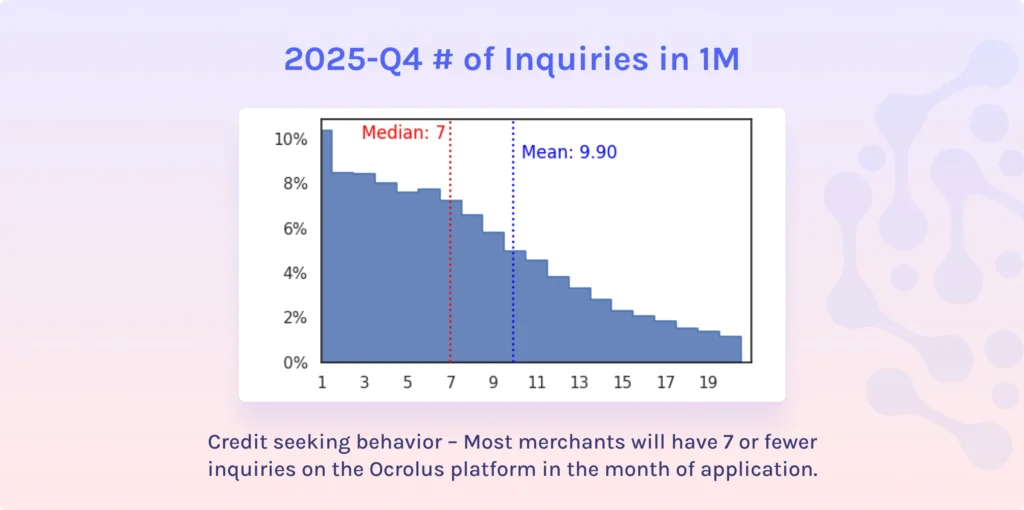

Loan inquiries show how often a merchant has appeared across the Ocrolus network over configurable time windows, including the last 30, 60, 90 days and up to a year. This provides immediate visibility into application velocity and credit-seeking behavior.

In practice, this helps underwriters answer questions that are often difficult to verify through documents alone:

- Is this merchant actively shopping for capital?

- Is application activity accelerating or slowing?

- Does recent behavior resemble prior spikes in credit demand?

Network data from 2025 shows that the median SMB appears between one and seven times in a one-month period, which is considered normal behavior. When inquiry counts rise significantly above that range or change rapidly over time, it can signal stacking risk, liquidity pressure or shifting borrower intent.

Because loan inquiries are resolved using Ocrolus’ entity matching and document processing infrastructure, they are based entirely on anonymized activity within the Ocrolus network, not external bureaus or third-party data sources.

Benchmarking adds peer context to cash flow analysis

Cash flow alone does not tell the full story. A business with strong revenue may still be underperforming relative to its peers, while a smaller business may be outperforming its industry.

Benchmarking within Ocrolus Intelligence addresses this challenge by comparing a merchant’s financial metrics to anonymized peer data from similar businesses in the same industry. Powered by NAICS classification enrichment, benchmarking delivers percentile-based insights that are immediately interpretable at the moment of underwriting.

Underwriters can see where a merchant’s revenue, expenses and other key metrics fall relative to peers, without performing manual research or relying on generic industry averages. This allows teams to validate assumptions, spot outliers and better understand whether performance is truly strong, weak or simply typical for that segment.

Importantly, benchmarking is integrated directly into the Ocrolus dashboard. It is not a separate analysis step, which helps teams move faster while maintaining consistency.

Missed the Product Pulse live? Catch the replay here:

From macro trends to individual decisions

During the Product Pulse, Ocrolus experts Lokesh Borkar, Senior Product Manager, SMB and Patrick Shubert, SMB Analytics Lead, also shared aggregated SMB trends observed across the network in 2025. Revenue growth varied meaningfully by industry, with professional services and manufacturing showing strength, while accommodation and food services faced margin pressure due to rising expenses.

This macro-level insight becomes far more powerful when paired with individual merchant data. Ocrolus Intelligence allows lenders to understand not just how industries are trending overall, but how a specific borrower compares to peers within that context.

Over time, Ocrolus plans to expand benchmarking capabilities further, including geographic segmentation and historical trend views, allowing underwriters to assess whether a business is strengthening or weakening relative to its local market.

Built into underwriting workflows, not bolted on

A defining principle behind Ocrolus Intelligence is workflow alignment. Loan inquiries and benchmarking are available today through both the Ocrolus dashboard and API, embedded directly into existing review processes.

Underwriters do not need new tools, additional logins or separate research steps. Instead, borrower behavior and peer context appear alongside cash flow analytics, helping teams make faster, more confident decisions without sacrificing rigor.

For lenders seeking deeper analysis, Ocrolus also supports custom network-level studies, portfolio benchmarking and feature correlation analysis through partnership with account teams.

Why this matters for SMB lenders

SMB underwriting has historically lacked standardized behavioral and peer context. Ocrolus Intelligence changes that by turning network-scale data into decision-ready insights.

By combining precision AI, human-in-the-loop validation and vertically integrated analytics, Ocrolus continues to deliver regulatory-grade decision intelligence that helps lenders fund more businesses, faster and with confidence.

Key takeaways

- Loan inquiries surface borrower credit-seeking behavior directly inside SMB Books.

- Benchmarking adds peer-based context to cash flow analysis using anonymized industry data.

- Percentile-based insights help underwriters validate assumptions quickly.

- Ocrolus Intelligence is embedded into existing workflows via dashboard and API.

- Network-level data transforms isolated documents into decision intelligence.