The real fraud risk in SMB funding is the data you can’t verify

TL;DR: Fraud in SMB funding has evolved beyond document manipulation. The deeper risk is data integrity — borrower information that breaks down as it moves across brokers, funders and partner networks. Funders that combine document analysis, cash flow intelligence and channel-level controls are better positioned to approve more good deals with confidence.

Fraud in small business funding has changed. Document manipulation still exists, but it is no longer the whole story — or even the most dangerous part of it.

The bigger risk today is data integrity. Borrower information rarely travels a straight line from applicant to decision. It passes through brokers, marketplaces and partner funders, getting reformatted, reinterpreted and sometimes manipulated along the way. By the time an application reaches underwriting, the data may look clean on the surface while carrying significant gaps in trust underneath.

The threat is not always a bad actor submitting a fake bank statement. It is often something harder to detect: inconsistent, unverified or silently altered data entering a workflow that has no way to flag it.

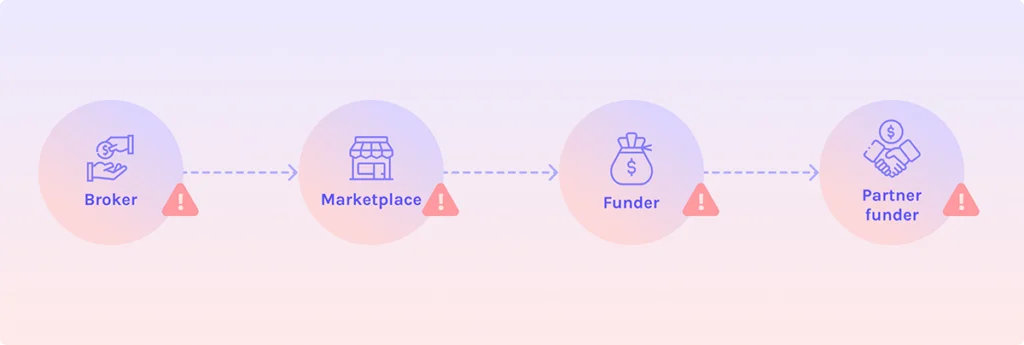

Why data breaks in transit

Most SMB funding workflows are still fragmented. A broker collects documents, runs a quick assessment and emails the file to a funder. That funder reprocesses the same documents, recalculates the same metrics and re-validates the application from scratch — not because the broker was dishonest, but because there is no shared standard of trust.

This duplication introduces friction. More importantly, it introduces risk.

In some cases, brokers collect digital bank data through connected account tools, then convert it to PDF before sending — stripping context, losing structure and creating openings for inconsistency. Each time data is touched or transformed, the likelihood of error or manipulation increases. Every handoff creates a gap.

The result is that funders are often not evaluating the borrower’s actual financial picture. They are evaluating a version of it — filtered through whoever handled the file last.

Where fraud actually shows up

Fraud in modern SMB funding does not live in one place. It surfaces across multiple layers, often in ways that individual document checks will miss.

Document-level anomalies — edited bank statements, missing pages, formatting inconsistencies — remain relevant. But cash flow tells a different story. Revenue patterns that do not align with deposits, irregular transaction behavior or sudden balance spikes can indicate manipulation that documents alone would never reveal. Ongoing cash flow monitoring adds another dimension entirely, surfacing risk signals that only become visible over time.

Then there is the data integrity layer. When different parties calculate income or revenue using different methods, conflicting versions of the same borrower story emerge. Without standardized interpretation across the ecosystem, funders are left reconciling those conflicts manually — or missing them entirely.

Finally, there is channel risk. Fraud patterns are often tied to submission sources. Repeated anomalies from specific brokers, unusual deal characteristics or declining data quality across a partner’s submissions are signals that aggregate-level visibility can surface — but only if the data infrastructure supports it.

What it takes to close the gap

Preventing fraud at this level requires more than flagging suspicious documents. It requires building trust into the data itself and the workflows it moves through.

That starts with standardization. When cash flow metrics are calculated and shared in a consistent format — one that all parties in the ecosystem can interpret the same way — funders can evaluate applications faster and with more confidence. Ocrolus cash flow analytics, trained on over 15 million applications, have become a shared standard that major SMB funders use to interpret bank data. That standardization is the foundation that makes cross-party trust possible.

It also requires layering signals. Document integrity checks, cash flow analysis and channel-level pattern detection each catch fraud that the others may miss. Evaluated together, they give funders a materially more complete picture of risk than any single layer can provide on its own.

Secure, permissioned data sharing eliminates a separate class of risk entirely. Encore, Ocrolus’s deal-sharing platform for SMB funding, addresses this directly — enabling funders and brokers to share verified cash flow profiles in real time through a double opt-in, standardized format. Rather than re-processing the same documents at every step, counterparties receive decision-ready data they can trust. That removes the handoff risk that fragmented broker and funder workflows introduce and reduces the surface area for manipulation.

Fraud prevention as a growth lever

The operational case for better fraud prevention is clear. Fewer bad deals enter the pipeline, losses decrease and compliance outcomes improve.

But the more important case is on the revenue side. When funders trust their data, they move faster. They approve more deals with confidence, reduce the rework caused by fragmented workflows and build stronger partner relationships over time. Cleaner data and more reliable networks lead to more predictable portfolio performance.

The goal is not only to stop bad deals. It is to fund more good ones—and to do so with the speed and confidence that competitive SMB funding demands.

Platforms like Ocrolus combine AI-powered document and cash flow analysis with secure, standardized data workflows to help funders reduce fraud exposure while increasing funding confidence across their networks. To learn more about Ocrolus, request a demo today.

Key takeaways

- Fraud in SMB funding is primarily a data integrity problem — inconsistent, unverified borrower data moving across fragmented ecosystems creates as much risk as deliberate document manipulation

- Every handoff between brokers, funders and partners introduces potential for data degradation, error or manipulation

- Effective fraud prevention requires layering document integrity checks, cash flow analysis and channel-level pattern detection — no single signal is sufficient

- Standardized cash flow metrics create a shared language of trust that enables faster, more confident funding decisions across the ecosystem

- Secure, permissioned data sharing platforms eliminate handoff risk and reduce the surface area for manipulation before deals reach underwriting

FAQ

What is data integrity fraud in SMB funding?

Data integrity fraud refers to risk that arises not from an obviously fake document, but from borrower information that has been inconsistently calculated, silently altered or degraded as it moves through brokers, marketplaces and partner funders. Unlike traditional document fraud, it is harder to detect because the data may appear structurally clean while carrying significant inaccuracies.

Why are fragmented SMB funding workflows a fraud risk?

When deals pass through multiple parties — each reformatting, recalculating or reinterpreting borrower data — there is no shared standard of trust. Each handoff creates an opening for inconsistency or manipulation. Fragmented workflows also encourage practices like converting digital bank data to PDF before sharing, which strips context and introduces additional risk.

How does cash flow analysis help detect fraud beyond documents?

Cash flow analysis examines transaction-level behavior — deposit patterns, revenue consistency, balance irregularities — that static documents may not reflect accurately. Revenue that looks solid on a bank statement can tell a different story when cash flow signals are analyzed in full, surfacing manipulation that document-level checks alone would miss.

What is channel-level fraud risk in SMB funding?

Channel-level fraud risk refers to patterns tied to specific submission sources — brokers or partners whose deals consistently show anomalies, declining data quality or unusual characteristics. This type of risk is only visible when deal data is analyzed in aggregate across a funder’s network rather than evaluated application by application in isolation.

What is Encore and how does it relate to fraud prevention?

Encore is Ocrolus’s deal-sharing platform for SMB funding. It enables funders and brokers to share verified cash flow profiles in real time through a secure, double opt-in format using standardized metrics. By replacing fragmented email-and-PDF workflows with trusted, decision-ready data, Encore reduces the handoff risk that creates openings for fraud and inconsistency.

Does AI replace human judgment in SMB fraud detection?

No. AI surfaces patterns and anomalies at a scale and speed that manual review cannot match, but human expertise remains essential for interpreting edge cases and making final credit decisions. The most effective fraud prevention approaches combine AI-powered analytics with human-in-the-loop validation to deliver both speed and accuracy.