Product Pulse recap: Automating rental income validation with the Fannie Mae income calculator

TL;DR: Rental and self-employed income are among the most complex areas of mortgage underwriting. Ocrolus integrates directly with Fannie Mae’s Income Calculator to deliver automated, GSE-eligible income assessments that qualify for rep and warrant relief — all within your existing workflow.

In this month’s Product Pulse, we walked through one of the most requested topics in mortgage underwriting from our customers: how Ocrolus automates rental and self-employed income validation through a direct integration with Fannie Mae’s Income Calculator. If you missed the live session, here is a recap of what we covered.

Income calculation is one of the most time-consuming and error-prone elements of mortgage underwriting, particularly for self-employed and rental income. Manual processes lead to delayed loan closings, compliance risks, miscalculations and increased buyback exposure. For lenders managing high volumes of complex files, the cost of that inconsistency adds up fast.

Ocrolus eliminates that inconsistency. By integrating directly with Fannie Mae’s Income Calculator, Ocrolus delivers automated income assessments eligible for rep and warrant relief, without requiring underwriters to leave their existing workflow.

Watch the replay below:

How it works

The Ocrolus and Fannie Mae integration is designed to fit inside the underwriting process, not around it. Here is how a file moves through the workflow:

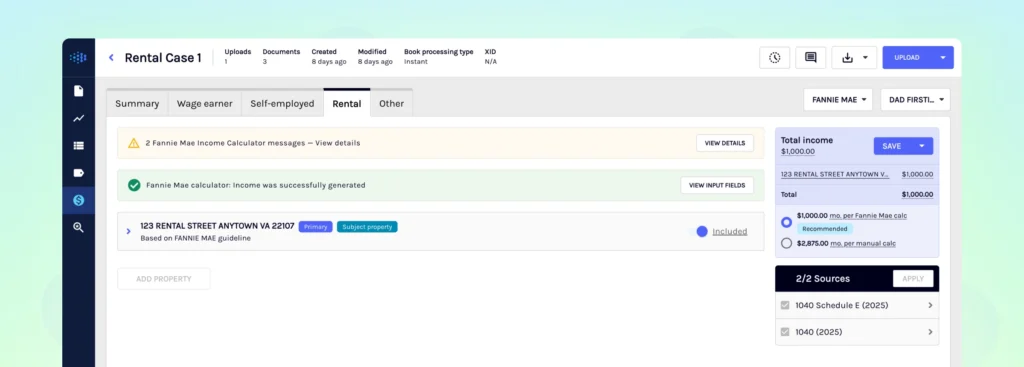

Borrower income documents are submitted via Ocrolus, where they are digitized and structured automatically. That data is then sent directly to Fannie Mae’s Income Calculator for processing. Results return to the Ocrolus Dashboard, clearly labeled and ready for review. From there, validated income values and case file IDs sync automatically to Encompass, along with any relevant alerts.

Underwriters stay in their primary system throughout. There is no re-keying, no tool switching and no manual tracking of case identifiers outside the core workflow.

Why this matters for rental income

Schedule E income analysis has always required careful judgment: tax return review, add-back calculations and property-level expense analysis. When that work happens manually, across different team members and branches, the results vary. A missed adjustment or undocumented override may not surface until quality control or post-close review, and by then, the file is much harder to defend.

The Ocrolus integration addresses this directly. Income amounts are calculated by Fannie Mae, not derived from manual math. Required data elements like employment start date, subject property designation and key rental expense inputs are enforced before submission, blocking incomplete files from moving forward. When documents change, re-runs are supported without disrupting the rest of the file.

The result is a structured, auditable baseline for every calculation; one that holds up under post-close scrutiny.

Key benefits

- Improved accuracy. Ocrolus reduces the need for manual document review and income calculation. With over 99% document analysis accuracy across all formats and quality levels, the data going into Fannie Mae’s Income Calculator is clean from the start.

- Increased confidence. Income amounts are calculated by Fannie Mae, not estimated by an underwriter working from a spreadsheet. Rep and warrant relief minimizes risk exposure and gives operations teams a defensible record for every file.

- Enhanced efficiency. Automated calculations run within existing workflows. Seamless integration with Encompass means underwriters import results directly rather than re-entering values, and case file IDs sync automatically for audit tracking.

- GSE compliance built in. The integration aligns with GSE-compliant guidelines and minimizes friction and regulatory risk by enforcing required inputs before any calculation is submitted.

A smarter workflow for complex income

Ocrolus is an AI-driven workflow platform that helps mortgage professionals, from loan officers to underwriters, make faster, smarter, and more confident decisions. Our technology automates the time-consuming document and data tasks that slow down origination, while keeping humans firmly in control of credit decisions. We use AI to extract and validate data from over 1,700 document types, then apply that intelligence to streamline workflows, like income (and conditioning) analysis, so lenders can focus on higher-value work.

Ocrolus is purpose-built for the complexity of mortgage underwriting. The Fannie Mae Income Calculator integration is a direct extension of that capability — bringing GSE-eligible calculation inside the workflow so lenders can move faster, reduce repurchase risk and build files that are easier to defend from the start.

Key takeaways

- Manual income calculation creates downstream risk. Delayed closings, miscalculations and buyback exposure all trace back to inconsistent manual processes.

- Ocrolus integrates directly with Fannie Mae’s Income Calculator. Income assessments are calculated by Fannie Mae and qualify for rep and warrant relief.

- The workflow stays intact. Documents go in via Ocrolus, results come back to the dashboard and validated values sync automatically to Encompass.

- Guardrails prevent incomplete submissions. Required fields are enforced before calculation, reducing downstream corrections and strengthening audit readiness.

- Over 99% document analysis accuracy. Clean inputs mean reliable outputs — and more defensible files at every stage of review.

Ready to streamline your mortgage income calculations? Schedule a demo to see how Ocrolus automates rental income validation inside your existing workflow.