Fraud in SMB lending has evolved. Your detection strategy should, too.

TL;DR: Fraud in SMB lending has evolved beyond forged bank statements into layered schemes involving synthetic cash flow patterns and identity manipulation. Most lenders have strong controls at intake but limited detection coverage downstream. That gap is where modern fraud lives. This post examines how multi-layer signal detection across the full borrower journey closes that exposure and what credit teams can do to address it.

Most SMB lenders can catch a forged bank statement. The problem is that fraud has moved somewhere else.

Document manipulation at intake remains real, but it’s no longer the source of the most damaging losses. Fraudsters have adapted, constructing synthetic cash flow patterns that pass surface-level review, layering identity signals across the application and exploiting handoff gaps between origination and funding. The lenders absorbing the biggest hits today aren’t missing obvious fakes. They’re operating with strong front-door controls and almost no detection coverage beyond them.

How fraud moved past the front door

The shift happened gradually. As lenders strengthened document review at origination by adding verification steps, flagging formatting inconsistencies and running statements through automated tools, fraudsters moved to softer targets.

Today’s most sophisticated SMB fraud blends legitimate and manipulated data in ways that clear standard controls. Synthetic cash flow manipulation is the clearest example. Rather than substituting a real statement with a fabricated one, operators alter transaction histories to reflect patterns that look credible: consistent deposit intervals, believable payroll cadences, minimal NSF activity. The manipulation is subtle enough to survive a quick manual review and invisible to detection tools focused only on document-level signals.

Identity layering compounds the problem. Fraudulent borrowers increasingly combine real business credentials with synthetic owner profiles, real account structures with altered transaction histories. The result is an application that passes every checkpoint cleanly, until a funded deal turns fraudulent and the loss has already been absorbed.

The detection gap most lenders don’t know they have

Most credit teams share a version of the same problem: intake controls are reasonably strong, but detection coverage ends roughly where the application does. Fraud that enters through the origination channel, a broker relationship or documents submitted before formal underwriting begins often goes undetected because no mechanism exists to surface it at that stage.

The consequences surface later. A lender’s cash flow analysis may reveal deposit inconsistencies that should have triggered review earlier in the process. Suspicious transaction patterns that an experienced underwriter would flag in isolation get buried in a deal that otherwise passes. By the time the fraud is visible, the deal is funded.

The Federal Reserve’s Small Business Credit Survey consistently identifies credit risk as a primary concern for small business lenders, and fraud that mimics legitimate creditworthiness is among the most difficult to screen.

The detection gap reflects a structural limitation: checkpoint-based controls at intake with no connected signal detection downstream. Closing it requires moving to pattern-based detection that operates across the entire underwriting journey.

What multi-layer detection looks like in practice

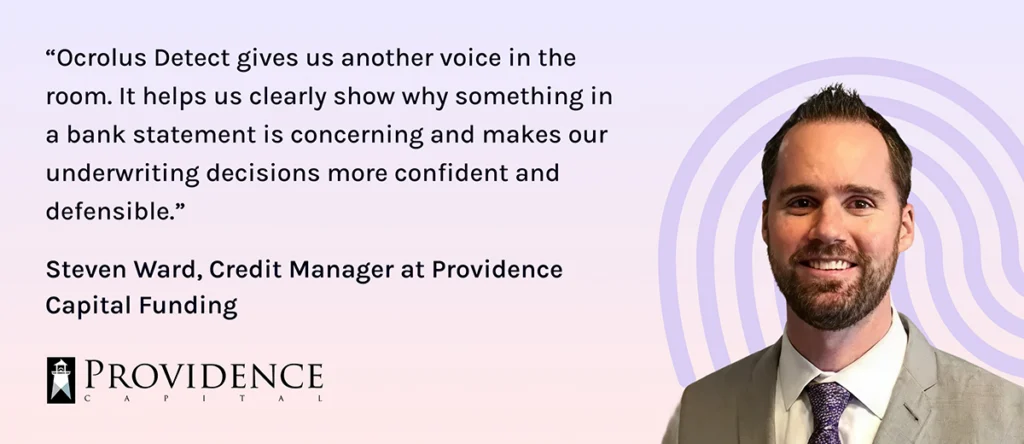

The most effective response layers automated signal detection on top of experienced human review. Providence Capital Funding, an equipment financing company with more than 20 years in SMB lending, built its detection program around this approach.

Before adopting Ocrolus Detect, the team relied primarily on manual bank statement review. It worked until fraud tactics became sophisticated enough to clear experienced analysts. “You might notice formatting inconsistencies or unusual transaction activity,” said Steven Ward, Credit Manager at Providence Capital, “but without objective signals, it can be difficult to clearly demonstrate why a file is problematic.”

After implementing Detect, AI-powered fraud signals surfaced automatically on every review: suspicious file origins, editing activity and potential document manipulation identified before underwriting moved forward. The change shifted how the team communicated risk decisions across credit and sales. “Instead of relying only on experience, we can point to the data and say this is what the signals are showing,” Ward said.

Fraud in SMB lending will continue to evolve. Detection strategies built for the threats of five years ago, focused on document authenticity at intake, leave real exposure in the gaps between application submission and funding.

The lenders best positioned to manage this risk treat fraud detection as a continuous process across the borrower journey, not a single checkpoint at the door. For credit teams still relying primarily on manual review, the question isn’t whether the detection gap exists. The question is how much it has already cost them and what closing it would change.

Key takeaways

- Fraud in SMB lending has shifted from document forgery at intake to layered schemes involving synthetic cash flow patterns and identity manipulation.

- Most lenders have strong front-door controls but little detection coverage after application submission. That gap is where modern fraud operates.

- Synthetic cash flow manipulation is designed to pass surface-level review; catching it requires pattern-based analysis across transaction data, not just document verification.

- Multi-layer detection combines automated signal surfacing with experienced human review, giving credit teams objective data to support and communicate risk decisions.

- Treating fraud detection as a continuous process across the borrower journey, not a single intake check, is the structural shift that closes material exposure.

FAQs

What is synthetic cash flow fraud in SMB lending?

Synthetic cash flow fraud involves manipulating transaction histories in bank statements to reflect patterns that appear legitimate: consistent deposits, believable payroll activity, minimal overdrafts. Unlike outright document forgery, the manipulation is subtle enough to clear standard document review and is only detectable through pattern-based analysis of transaction data over time.

Why are SMB lenders vulnerable to fraud after application intake?

Most SMB lenders concentrate fraud controls at origination, verifying documents and checking for obvious manipulation, but have limited coverage for fraud that enters through broker or ISO channels or that only becomes visible during underwriting. This creates a detection gap between where controls exist and where fraud actually operates.

How does multi-layer fraud detection work in SMB lending?

Multi-layer fraud detection combines automated signal analysis, scanning documents for suspicious file origins, editing activity and transaction anomalies, with experienced human review. Rather than relying on a single checkpoint, it creates overlapping coverage across the full underwriting journey, making it harder for sophisticated fraud to clear all detection mechanisms.

What signals does AI-powered fraud detection look for in bank statements?

AI fraud detection tools analyze bank statements for document-level signals (suspicious file origins, editing activity, formatting inconsistencies) and transaction-level signals (unusual deposit patterns, cash flow anomalies, NSF behavior inconsistent with reported revenue). Together these signals produce a more complete picture of fraud risk than manual review alone.

How does Ocrolus Detect help SMB lenders catch fraud?

Ocrolus Detect analyzes uploaded bank statements using AI-powered fraud signals to identify potential document manipulation, suspicious file activity and transaction anomalies. It surfaces these signals automatically during underwriting, giving credit teams objective, data-backed indicators to support more confident and consistent fraud risk decisions.