Why automated conditioning is the key to faster clear-to-close

TL;DR: Automated conditioning shifts discrepancy detection to document ingestion — before files ever reach the underwriting queue — rather than during manual review. Ocrolus flags income mismatches, documentation gaps and data inconsistencies early, so underwriters clear files instead of generating new borrower requests. Lenders that deploy automated conditioning report fewer last-minute conditions, stronger pull-through rates and faster clear-to-close timelines.

The average mortgage takes more than 40 days to close, and a disproportionate share of that time is lost not to appraisals or title work but to conditions. Each condition triggers a new round of borrower outreach, document collection and re-review. By the time a file is clear to close, it may have cycled through two or three condition rounds. The problem isn’t that conditions exist — they’re a necessary control in sound underwriting. The problem is when they surface late, after the borrower has already assumed the finish line is near. Automated conditioning addresses this by moving discrepancy detection to the earliest stage of the process, before files ever reach the underwriting queue.

When conditions surface late, everyone loses

Conditions are a function of information gaps. An underwriter reviewing a file finds a paystub that doesn’t reconcile with the W-2, a bank statement showing a large undocumented deposit or an income calculation that doesn’t align with the 1003. Each finding generates a condition. The borrower gets a request. The file sits while the lender waits. If the response comes back incomplete, the cycle repeats.

This late-stage discovery pattern is a primary driver of extended cycle times. Industry origination data consistently shows that loans requiring multiple condition rounds take materially longer to close and are more likely to fall out of the pipeline entirely. Pull-through suffers not because borrowers don’t qualify, but because they disengage when the process stalls unexpectedly.

The root cause is a reactive review structure. Without automated analysis running ahead of human review, discrepancies sit undetected until an underwriter opens the file — often days or weeks after the borrower assumed the process was nearly done.

Early discrepancy detection changes the condition math

Automated conditioning moves the detection window to document ingestion. Rather than waiting for an underwriter, the platform analyzes documents as they arrive — cross-referencing income figures against amounts stated on the application, flagging inconsistencies between W-2s and paystubs and identifying documentation gaps before a file enters the queue.

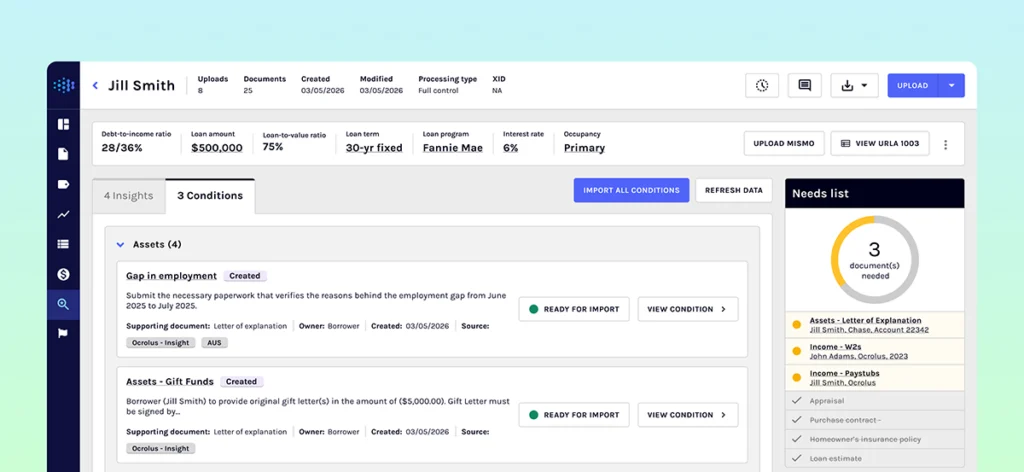

Ocrolus applies this by running document-level and data-level validation at submission. When a paystub’s year-to-date figure doesn’t align with the monthly income on the application, the system flags it immediately. When required documents are missing or illegible, the borrower can be notified earlier in the process — before the file ever reaches the underwriting queue. By the time an underwriter opens the file, the most common condition triggers have already been surfaced, categorized and queued for resolution rather than waiting to be discovered.

The practical effect is a shorter underwriting queue. Files arrive more complete, require fewer condition rounds and move toward clear-to-close faster. Underwriters spend their time on credit judgment, not document chasing. Each condition surfaces with the relevant Fannie Mae or Freddie Mac selling guide reference attached, so underwriters have the guideline context they need without manual lookup. On complex income scenarios — self-employed borrowers, rental income, multiple employers — where multiple document types interact, early validation has an outsized impact on how often last-minute surprises derail a file at closing.

LOS integration makes automated conditioning operational

Detection only improves pull-through if it fits into how lenders actually work. Most mortgage operations run through a loan origination system like Encompass, and any automation layer has to work within that infrastructure, not around it.

Ocrolus integrates directly with major LOS platforms, surfacing condition flags and document validation results inside the systems underwriters already use. There’s no separate login, no additional workflow step, no data export. The analysis runs at ingestion and results appear where underwriters expect to find them.

LOS-native integration also supports defensible audit trails. Every discrepancy flagged and every condition surfaced through automated review is documented, timestamped and tied to a specific data point in the file. When QC teams or regulators review a loan post-close, the decision logic is traceable — not reconstructed from memory. For lenders operating in a regulatory environment that demands documentation of credit decisions, that auditability matters as much as the speed.

Clear-to-close is the moment a loan is approved for the closing table. Getting there faster isn’t just a competitive advantage — it determines whether the deal closes at all. Borrowers who encounter repeated conditions and extended timelines disengage. Lenders who catch issues early protect pull-through rates and keep origination costs in check.

Automated conditioning doesn’t eliminate the need for human underwriting judgment. But it changes what underwriters encounter when they open a file. When the most common discrepancies are surfaced at ingestion, conditions become the exception rather than the rule — and closing timelines reflect that.

Key takeaways

- Late-stage conditions are one of the primary drivers of extended mortgage cycle times and elevated fallout rates — catching discrepancies early is the most direct lever lenders have on pull-through.

- Automated conditioning analyzes documents at ingestion, flagging income mismatches, undocumented deposits and documentation gaps before files reach the underwriting queue.

- Ocrolus runs document-level and data-level validation at the point of submission, giving underwriters cleaner files and reducing the rounds of borrower outreach required to clear conditions.

- Each condition surfaces with the relevant Fannie Mae or Freddie Mac selling guide reference attached, eliminating manual guideline lookup and standardizing how conditions are documented across teams.

- LOS integration ensures automated conditioning works within existing workflows — condition flags surface inside the systems underwriters already use, with no additional logins or parallel processes.

FAQs

What is automated conditioning in mortgage underwriting?

Automated conditioning is the use of AI-driven document analysis to identify data mismatches, documentation gaps and income inconsistencies at the time of document submission — before files reach an underwriter. Rather than waiting for a human reviewer to find problems, the platform flags them immediately, allowing lenders to resolve issues earlier and generate fewer last-minute conditions.

How does automated conditioning speed up clear-to-close?

By catching discrepancies at ingestion, automated conditioning reduces the number of condition rounds required during underwriting. Files arrive at the underwriting queue more complete, borrower outreach happens earlier in the process and underwriters spend less time generating new requests. The result is a compressed review cycle and a faster path to clear-to-close.

What kinds of discrepancies does automated conditioning catch?

Common flags include paystub year-to-date figures that don’t reconcile with stated monthly income, bank statements showing undocumented large deposits, W-2 and paystub inconsistencies and missing or illegible required documents. For complex borrowers — self-employed, rental income, multiple employers — the system validates across multiple document types simultaneously.

How does automated conditioning integrate with a loan origination system?

Ocrolus integrates directly with Encompass and other LOS platforms, so condition flags and validation results surface inside the systems underwriters already use. There is no separate login or workflow. Flags appear in context, with documentation tied to specific data points in the file and relevant Fannie Mae or Freddie Mac selling guide references attached.

Why does the timing of condition discovery matter for pull-through?

Conditions surfaced late in the process — after a borrower believes the loan is nearly approved — create friction that drives disengagement. Each new round of document requests extends the timeline and increases the likelihood the borrower walks. Early detection gives lenders the opportunity to resolve issues when the borrower is still fully engaged, protecting pull-through rates.